Alternative Assets in 2024 Annual Review: Navigating Private Markets Vortex

- Marie-Laure Mikkelsen

- Mar 5

- 6 min read

State of the Industry Series: Fund Selector Talk I-2025 - Alternative Assets Review in 2024

The private markets have shown gradual improvement amid a challenging economic backdrop. While managers have faced persistent headwinds, the year has also highlighted the resilience and adaptability of these asset classes. Private markest continue to offer portfolio diversification opportunities for each risk profile.

I. Private Equity in 2024: A Year of Patience and Innovation

Private equity firms entered 2024 with a sense of anticipation. Falling interest rates and improving stock market valuations signaled a potential turning point after a period of uncertainty. However, the surge in M&A and buyout activity didn't materialize to the extent that many had anticipated. While global buyout deal value climbed by more than a third over the first nine months of 2024, it remained well below the peak levels of 2021.

The challenge was particularly acute when it came to exits. At the end of Q3 2024, global exit value was down nearly a third compared to the same period last year. Landing exits at attractive valuations remained the biggest hurdle for private equity firms, impacting distributions to investors and, consequently, fundraising efforts. PEI figures show that private equity fundraising fell to its lowest level in four years during the first three quarters of 2024.

The fundraising landscape became increasingly concentrated, with a small group of large managers absorbing much of the available capital. The ten largest buyout funds that closed in the first half of 2024 accounted for almost two-thirds of the capital raised. This trend reflects a preference among investors for established managers with scale and a proven track record in navigating volatile markets.

Faced with these challenges, private equity demonstrated its adaptability. The secondaries market thrived, providing an essential source of liquidity for managers and investors seeking to unlock value in a cash-constrained environment. Secondaries deal value reached a record in the first half of 2024.

Furthermore, innovative financing solutions like NAV financing and dividend recaps gained traction, offering alternative avenues for generating distributions and supporting portfolio companies. While the reopening of primary exit channels will be crucial for reigniting fundraising, 2024 showcased the resilience and ingenuity of the private equity industry.

To thrive in this environment, private equity managers need to be proactive in sourcing liquidity, embrace innovative financing solutions, and demonstrate their ability to add value beyond traditional exit strategies.

II. Private Debt in 2024: Resilience Amidst Rising Competition

Private debt continued its strong performance in 2024, delivering attractive risk-adjusted returns and attracting significant investor interest. Fundraising remained robust, with Private Debt Investor figures showing only a fractional decline compared to the record levels of 2023. This resilience stems from the consistent returns and stability that private debt offers.

Research highlights the strong historical performance of direct lending strategies, which have outperformed both leveraged loans and high-yield bonds since 2008. Moreover, private credit portfolios have weathered the rising interest rate environment well, with default rates remaining relatively low. The overall private credit default rate was below percent in Q3 2024.

This stability reflects the strength of the private credit model, where managers conduct thorough due diligence, maintain focused portfolios, and work closely with borrowers. However, the reopening of broadly syndicated loan (BSL) markets presented a new challenge. As interest rates declined, BSL issuance surged, offering cheaper financing options and winning back some borrowers from private credit.

Private debt funds responded by adjusting their pricing and emphasizing their ability to provide flexibility, speed of execution, and reduced syndication risk. While competition from BSL markets is likely to persist, private debt remains an attractive asset class for investors seeking consistent income and downside protection.

To maintain their competitive edge, private debt managers need to focus on flexibility, speed of execution, and strong relationships with borrowers, while also carefully managing margins in a more competitive environment.

III. Real Assets in 2024: Unearthing Opportunities in a Shifting Landscape

Real assets faced a mixed environment in 2024. Despite cooling inflation and interest rate cuts, fundraising for real estate and infrastructure funds remained subdued. PERE data shows a significant decline in real estate fundraising, while Infrastructure Investor reports that full-year figures for infrastructure fundraising could fall short of 2023 levels.

This cautious approach reflects lingering uncertainty surrounding the impact of geopolitical tensions and the US presidential election on long-term real asset performance. However, green shoots emerged in the real estate sector in the second half of the year, with reported improvement in transaction activity driven by lower debt costs and increased pricing clarity.Large, developed markets like the US and UK led the rebound, with sectors like hospitality, retail, and office showing signs of recovery. In infrastructure, deal activity varied by subsector, with power and transport experiencing strong growth, according to CBRE.

Two megatrends continued to shape the real assets landscape: data centers and decarbonization. Investment in data centers remained robust, fueled by the insatiable demand for data to support digitalization and AI. The US colocation data center market has more than doubled in size in the past four years.

Decarbonization also emerged as a key priority, driven by regulatory pressures like the Sustainable Finance Disclosure Regulation (SFDR), higher energy efficiency standards and the need to reduce emissions in the construction environment. This presents significant opportunities for investors and developers to create sustainable and high-performing real estate portfolios. Real estate investors are increasingly focused on transitioning to lower-emission buildings, presenting significant opportunities for differentiated portfolios and higher returns. Similarly, investors across the real asset spectrum should prioritize sectors with strong growth potential, such as data centers and renewable energy, while also carefully assessing risks related to geopolitical tensions and economic volatility.

Looking ahead, real assets managers will continue to rely on these megatrends while hoping that lower interest rates can revitalize other segments of the market in 2025.

IV. Hedge Funds: Navigating Volatility and Seeking Alpha

Hedge funds entered 2024 navigating a complex landscape of macroeconomic uncertainty, shifting interest rates, and evolving investor expectations. The year was marked by a focus on alpha generation and risk management, as managers adapted to volatile markets and sought to differentiate themselves in a crowded field.

Quantitative hedge funds continued to gain traction in 2024, leveraging advancements in artificial intelligence (AI) and machine learning to refine their models. These funds outperformed in environments where traditional fundamental analysis struggled to keep pace with rapid market movements. However, the increasing reliance on quantitative strategies also raised concerns about crowded trades and systemic risks, particularly in highly liquid markets.

Hedge fund performance in 2024 was mixed, with dispersion across strategies. According to industry reports, equity long/short funds faced headwinds due to uneven stock market performance, while event-driven and credit strategies delivered more consistent returns. Despite these challenges, hedge funds remained a key component of institutional portfolios, offering diversification benefits and downside protection in volatile markets.

Investor sentiment toward hedge funds was cautiously optimistic. While some allocators remained critical of high fees and inconsistent performance, others appreciated the asset class’s ability to generate uncorrelated returns. Fundraising trends reflected this dichotomy, with inflows concentrated on top-performing managers, niche strategies such as climate-focused and ESG-aligned funds and the demand for customized solutions.

Looking ahead, hedge funds face both opportunities and challenges, including increased competition and regulatory scrutiny. Rising competition from private markets and passive investment vehicles has intensified pressure on fees and performance. At the same time, technological advancements, the growing complexity of global markets and market dislocations present new avenues for alpha generation.

Managers who can adapt to these dynamics—while delivering consistent, risk-adjusted returns— and build trust with investors through transparency and communication are likely to thrive in the years to come.

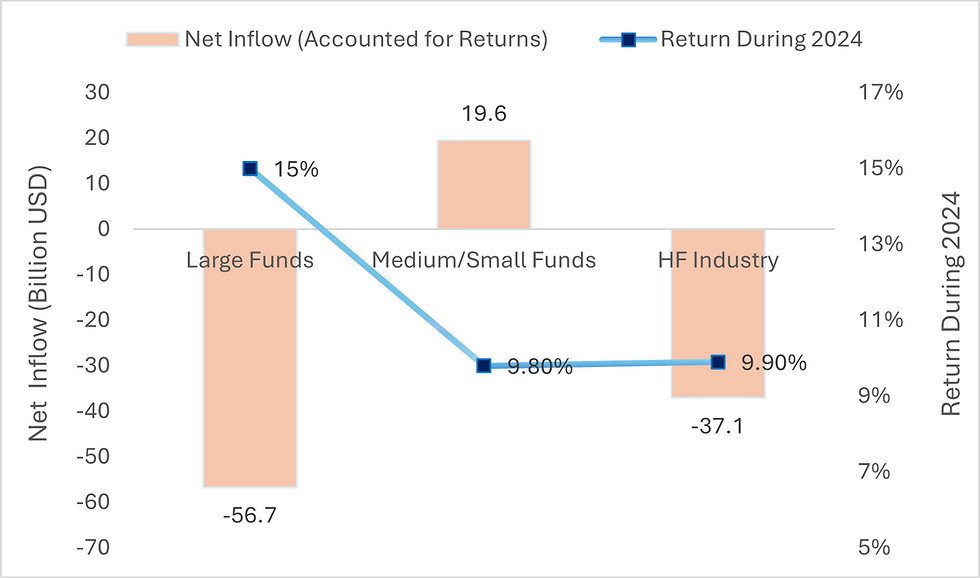

The hedge fund industry experienced a total net outflow of $37.1 billion in 2024, adjusted for the positive 2024 returns, with an unexpected shift away from the largest Hedge Funds smaller hedge funds.

Conclusion:

2024 was a year of adaptation and innovation for alternative assets. Private equity demonstrated resilience by embracing alternative liquidity solutions and financing strategies. Private debt navigated rising competition from BSL markets by emphasizing flexibility and strong borrower relationships. Real assets focused on megatrends like data centers and decarbonization to unearth opportunities in a shifting landscape. And hedge funds continued to evolve, seeking alpha and meeting the evolving needs of investors.

As we look ahead to 2025, the lessons of 2024 will be critical but alternative assets are poised to play an increasingly important role in diversified portfolios. Managers must continue to innovate, offering creative liquidity solutions and differentiated value propositions to navigate the denominator effect and evolving market dynamics. For investors, the year has reinforced the importance of patience and selectivity, as private markets remain a vital component of long-term portfolio strategy. While challenges persist, the adaptability demonstrated in 2024 offers a strong foundation for growth in the years to come.

Disclaimer Please note that articles may contain technical language. For this reason, they may not be suitable for readers without professional investment experience. Any views expressed here are those of the author as of the date of publication, are based on available information, and are subject to change without notice. Individual portfolio management teams may hold different views and may make different investment decisions for different clients. This article does not constitute investment advice. It is provided for information purposes only and does not constitute an invitation to invest. Please seek advice from your investment advisor before investing.

Comentarios